The GST refund process is no longer difficult as the government has introduced an alternative process for filing GST refund claims manually for exporters. This process will be faster and the refunds will be processed within seven days.

Under GST, the exports of taxable goods or services are treated as zero-rated supplies. It means that the suppliers will not have to pay any GST tax on any of their exports. However, imports are taxable under the new tax regime. Exporters can claim refunds of their input tax paid on imports. The process is, however, a little cumbersome.

Until now, the refund claim was to be filed online on the common portal. It was a long and tricky process The untimely supply of input credits has greatly affected the liquidity of such exporters whose businesses are completely dependent on the continuous and regular flow of cash. Things are now likely to get much easier as the government has allowed exporters to manually find refund claims.

Latest Update

- The GST Council has decided to remove the threshold limit on refunds for low-value export consignments, benefiting small exporters using courier and postal modes. View more

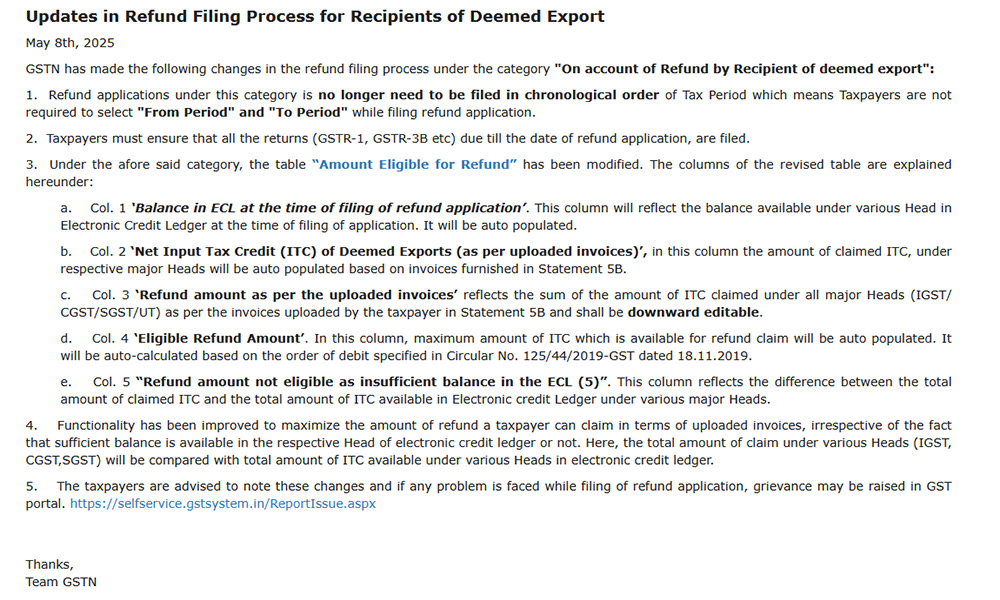

- New changes have been made to the refund filing process by GSTN on account of refunds claimed by recipients of deemed exports. View more

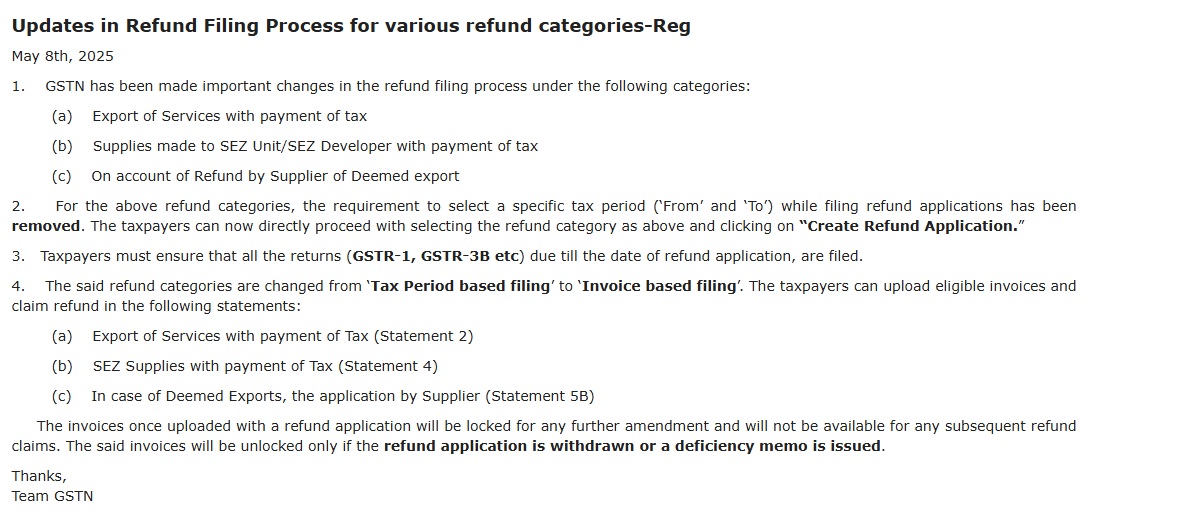

- The GST department has made changes to the refund filing process in various categories. View More

47 GST Council Meeting Updates

- “Change in the formula for calculation of refund under rule 89(5) to take into account utilisation of ITC on account of inputs and input services for payment of output tax on inverted rated supplies in the same ratio in which ITC has been availed on inputs and input services during the said tax period. This would help those taxpayers who are availing ITC on input services also.”

- “a. Amendment in CGST Rules for the handling of pending IGST refund claims: In some cases where the exporter is identified as a risky exporter requiring verification by GST officers, or where there is a violation of provisions of the Customs Act, the refund claims in respect of export of goods are suspended/withheld.”

- “Amendment in rule 96 of the CGST Rules has been recommended to provide for transmission of such IGST refund claims on the portal in a system-generated FORM GST RFD-01 to the jurisdictional GST authorities for processing. This would result in expeditious disposal of such IGST refund claims, after due verification by GST officers, thus benefitting such exporters.”

- “In respect of refunds about supplies to SEZ Developer/Unit, an Explanation to be inserted in sub-rule (1) of rule 89 of CGST Rules to clarify that “specified officer” under the said sub-rule shall mean the “specified officer” or “authorised officer”, as defined under SEZ Rules, 2006.”

- “Amendment in CGST Rules to provide for refund of unutilized Input Tax Credit on account of Export of Electricity. This would facilitate the exporters of electricity in claiming a refund of utilised ITC on zero-rated supplies.”

- “Time period from 01.03.2020 to 28.02.2022 to be excluded from the calculation of the limitation period for filing a refund claim by an applicant under sections 54 and 55 of the CGST Act, as well as for the issuance of a demand/ order (by a proper officer) in respect of erroneous refunds under section 73 of the CGST Act. Further, the limitation under section 73 for FY 2017-18 for issuance of an order in respect of other demands linked with a due date of annual return, to be extended till 30th September 2023.”

How to File GST Refund Claims?

Exports that paid IGST and those who paid tax on inputs and those merchants who make zero-rated supplies to SEZ units can now claim refunds for their input credits.

In order to claim ITC, an exporter has to follow the steps mentioned below.

- Download the refund Form RFD-01A from the GST Portal, you can view also here, For English and For Hindi

- Fill in the form providing the correct details

- Submit the form to the Jurisdictional Commissioner of your area

“Due to the non-availability of the refund module on the common portal, it has been decided by the competent authority … that the applications/documents/forms pertaining to refund claims on account of zero-rated supplies shall be filed and processed manually till further orders,” the CBEC said in a circular.

As of now, the option for filing refund claims is not activated on the GST Portal website. The CBEC only last month started the refund process for exporters who have paid IGST and filed refund claims through the GST Portal.

From now on, exporters will have to download and manually file Form RFD-01A in order to claim input credit for the IGST paid by them. The form has to be printed and submitted to the Chief Commissioner of Central Tax and the Commissioner of State Tax.

The tax refund, upon successful verification, will be granted by the tax officer within 7 days.

Exporters making supplies to SEZ units and those who have paid GST inputs will also be eligible to claim refunds through the manual system. However, the clarification regarding the timeline (and by when the exporters will receive the refund in their bank accounts) is still not clear.

Claim Refunds Through GSTR 2A Printout

The finance ministry recently announced that now the taxpayers can claim the refunds directly by showing up the GSTR 2A form printout to the concerned tax authority and the officials will initiate the refund disbursal procedure as soon as possible. Earlier, the invoice was required for each and every transaction for claiming the refund but now the ministry has limited the proof validation through the GSTR2A form only.

The complete details can be sorted out from here while the finance ministry will be issuing a formal notification in this regard as soon as possible.

Minister Claims Taxes Easy to Pay But Difficult to Get Refund

In a recently held exports excellence awards ceremony organized by FIEO (Federation of Indian Export Organisations) Eastern Region, West Bengal finance minister Amit Mitra stated that the refund delivery mechanism under the GST has gone more primitive than earlier due to the manual processing of refund application. The cited reason was the lower interfacing between the GST Network (GSTN), the electronic data interchange (EDI) and the Directorate General of Foreign Trade (DGFT).

The minister said that “Even in the state VAT system, there was no manual intervention in the entire process of filing of returns, It has been noticed that there is no interface between GSTN and DGFT EDI systems. Even the training given to the officers on the ground on issues like Letter of Undertaking (LUT) and related matters has not been adequate…it has been experienced that it is easy to pay tax but it is very difficult to get a refund.”

The reports stated that the refund of IGST paid on goods exported ITC refund on exported goods under LUT in July August and September is still pending. The late refund may also impact adversely labour-intensive jobs in the export sector.

Online Process for GST Refunds

The above process is done manually but now the Indian government is also giving online facility to file refund forms for export transactions. Read PDF

Important FAQs on GST Refund Topic

Q.1 What could be claimed as a refund?

The tax, interest on these taxes, and the additional amounts or any other element could be eligible to claim as a refund when the same would be the qualified cases.

Q.2 What would be the qualified cases for claiming the GST refund?

- Tax Paid on Zero rated supply (tax paid on Export or SEZ supply)

- The unused Input Tax Credit (‘ITC’) if export/sez supply is incurred with tax payment or Invert duty structure case.

- Tax Paid on Invoice in which the supply would not make, and refund voucher has been provided.

- Incorrect head tax paid (CGST & SGST instead of IGST and vice versa)

- Excess Cash ledger balance

- Tax, Interest, or any additional amount paid and incidence of such tax, interest not passed to any other individual

The common refund circumstances would be the export/ sez supply, Invert Duty Structure, and excess cash ledger balance

Q.3 Is there any time limit for the Refund application?

It is two years from the related date

Q.4 Is there any time limitation for allocating the Refund Order?

60 days from the receipt date of application finished for all concerns.

Q.5 Because of Covid-19 is there any ease in the timeline to furnish the GST refund?

For the analysis of 2 years notification 13/2022 on 5th July 2022, the period from 01-03-2020 to 28-02-2022 would not be included.

Q.6 In the case of Export supply, the input of Capital goods can be claimed as a refund?

No, excluding the capital goods, the exporter supply without the tax payment could merely claim for the refund of the input and input services that had been used in making these supplies. But the credit claim of taxes furnished on buying of the capital goods utlised for future course of business.

Q.7 What the term LUT means?

Any registered individual who claimed the option to supply goods or services for export /SEZs excluding any payment of integrated tax should file, prior to export/SEZs supply, a Letter of Undertaking (LUT).

Q.8 M India Pvt Ltd has valid LUT, are they enabled to export with payment of taxes?

Yes, despite holding a valid LUT the exporters are able to supply with tax payments.

Q.9 Can a person apply for LUT if he would have submitted Bank Guarantee for the issue of a Bond?

Yes, he is enable to submit LUT, and obtain the bond submitted which was released before.

Q.10 Are there any restricted goods wise where an Invert duty structure refund is not authorized?

Yes, for the concern of supply of nil-rated and fully exempted goods, there would be no GST refund towards Input tax credit on the input. Moreover, under the act nearly 45 HSN codes specified in which no ITC is being permitted, in which the credit has accumulated on the basis of the tax rate on inputs being higher as compared to the tax rate on the output supplies of these goods. For instance, HSN codes: 5007, 1507 to 1518, 2701 to 2703, 8601 to 8608, etc.

Q.11 Is there any other condition for the casual taxable individual or a non-resident taxable individual?

Yes, no refund would get permitted to the non-resident taxable individual or casual assessee until that individual files all the returns in relation to the whole duration for which the certificate of the registration allotted to him would be successively effective.

Q.12 As an export does the supply of services to Nepal would be treated?

Yes, through the RBI payment for the export of services to Nepal is permitted in Indian Rupees.

Q.13 Can the refund of TDS/ TCS in the cash ledger under section 51/52 be claimed?

Yes, under sections 51/52, the TDS/TCS amount can be credited in the electronic cash ledger along with any amount that would not be used inside the electronic cash ledger, post release of the tax dues along with the additional dues could get refunded to the individual.

Q.14 Can there be a refund of the compensation cess for the concern of export against IGST payment?

The compensation of the input tax credit might be taken towards the export supplies along with the refund of these unused input tax credits would be available. But the computation of the refundable amount of compensation cess will be performed separately along with the amount computed shall get completely debited through the compensation cess balance available in the electronic credit ledger. (refer to Circular No. 125/ 44/2019 dated 18th November 2019).

Q.15 Can adjustment of any demand get managed against a refund?

Yes, excluding the provisional refund the demand could be managed against the final refund.

Q.16 Is there any minimum limit for a refund?

Yes, beneath each tax head separately and not cumulatively, Rs 1000 would be the min limit for the refund.

Q.17 A person obtained an exemption from all obligations of customs on imports beneath EPCG, advance license, and others do these exemptions would indeed carry on for GST?

On the imports, the Holders of Advance Authorization / EPCG and EOUs would not be required to furnish the IGST, cess, and others.

Q.18 What is the type of invoices in which GSTR2A /2B conditions do not get applied?

For ISD Invoices, Imports invoices along with the inward supplies are responsible for Reverse Charge (RCM Supplies).

Q.19 Does a provisional refund is obligatory?

No there would not be any prohibition beneath the statute which makes a proper officer preventing from authorizing the complete amount.

Q.20 What are the essential circulars concerned with the refund?

- Circular No. 125/44/2019, dated 18th November 2019

- Circular No. 139/09/2020, dated 10th June 2020

- Circular No. 135/05/2020, dated 31st March 2020

- Circular No. 110/29/2019, dated 3rd October 2019

- Circular No. 147/03/2021, dated 12th March 2021

Q.21 Do unregistered Buyers claim a refund?

On the date of 17th December 2022, according to the press release of the 48th Meeting of the GST Council, no process would be there to claim for the refund of the tax that the unregistered purchasers take for the circumstance of the contract/ agreement for the supply of services, like construction of flat/house and long-term insurance policy, would get revoked as well as the time duration of the credit note issuance via related supplier would lapse. The department suggested the revision in CGST rules, 2017, and circular issuance, to specify the functionality for refund application filing via the unregistered purchasers in these cases.

{kind=link}

{kind=link}

{kind=link}

Respected Sir,

My total turnover is Export Turnover, my question is that I was exported the goods in FY 2017-18 & 2018-19 without filing LUT through the courier, but now I want to claim the Unutilised ITC for both years but while filing online refund application system ask for ARN of LUT, so in this case can I file the refund application manually?

Also, let me know the consequences of the non-filing of LUT, ut export is done.

LUT must be there if you want to file refund application, as without filing LUT GST portal may not allow you to file Refund form and for more detail please contact GST practitioner

Sir, I have made application for GST refund in LUT export in the month of Dec 2018, but by mistake I generated ARN without putting any amount means NIL refund ARN generated, then after I applied Jan 2019 refund application I have received refund for Jan 2019 but How can I make DEC 18 Reapplication for refund?

Dear Sir, when I upload JSON file of Rfd 01 in inverted data structures refund At that time “invalid data format” error display. Please help in this matter.

Dear Sir/Madam,

We are making export with payment of tax. But since long we are unable to get our IGST refund either our GSTR-1 or GSTR-3B data is correctly uploaded on the portal. Don’t know where is the problem and why the refund has stuck.

Please advise.

I have not filed the GST 3B return from Apr,18 to Sept, 18, my turnover is below 10 lakh. Every month I have paid the tax by calculating GSTR1-GSTR2. I have also filed GSTR1 every month from Apr,18 to Sept, 18. Kindly tell me how much fine, I will be paid for not filing the GST 3B from Apr,18 to Sept,18

You have to pay the late fee of Rs. 25/- per day in CGST and Rs.25/- per day in SGST from the due date of filing the return till the date return is filed.

Dear Sir,

Recently GST portal changes the format of GSTRFD-01A for export sales, now we have to upload the details of export bill and copy of bill in pdf format, and so please inform me about the procedure of filling of GSTRFD-01A online through the GST portal and further inform me about how much time to take to available of such GSTRFD-01A in your portal.

Thanking you

“Need your advice”

We have wrongly mentioned export sale amount(3.1.b) in total turnover column(3.1.a) in GSTR 3b due to this mistake we are not able to create refund application for refund with payment of IGST.we are export service provider and we are issuing only single invoice monthly and we have LUT so not charging IGST now.so how to claim refund.

In this case, make amendment in next GSTR-3B return showing export sale under the respective head and then claim refund thereof.

Sir,

Need your valuable advice, Wrongly paid tax to CESS Head & we claimed the refund to state tax authority with RFD Form manually, now they told us to fill online for an application. is it any separate procedure for CESS Refund? or is it like same as an Export procedure?

You can file RFD-01 online by login into gst.gov.in. Go to services Refunds Application for the refund and fill the necessary details.

What is the difference between old Rebate refund & GST rfd01?

We are an exporter who is into the supply of fabric and we have opted for scheme wherein we pay the GST and take the refund from the Port Authorities. But since we are taking the refund from the port authorities we have an accumulated input tax credit on Compensation Cess which we are not able to take a refund.

So we request you to advise us the process or way of getting the refund of Compensation Cess.

As per the rules under GST, provisions related to zero-rated supply in context to IGST paid on exports will also apply to compensation cess. So while claiming the refund of IGST on exports you can also claim the refund of compensation cess.

I have filed RFD01A for the refund but the officer has issued a discrepancy memo to me and asked to resubmit the RFD01A with rectification, can we do this now?? and if yes what is the procedure?

How to arrive “adjusted total turnover”? for Example Zero Rated Sales Rs.100000, exempt sales Rs.5000, State Sales Rs.7000. Please guide

We have exported goods in the month of August 2017 through merchant exporter who has deducted the segment of GST charged by us in the invoices and claims that he will pay the GST tax amount only after he has received from the GST authorities. We are manufacturers of MOULDS & DIES and our sizeable amount are held up since AUGUST 2017 which has affected seriously our working capital. No Bank is helping us.

This way we are afraid our working capital would be while away completely causing severe financial crunch to the detriment of our business. Please guide us as to what should we do under the circumstances.

Thanks and regards,

RUPESH SHARMA

Hi,

Carry forward of ITC is not allowed while claiming the refund of ITC in case of zero-rated supply. for example, the GSTN does not allow a claim of ITC for July, if purchases happen in one month (say July) and exports happen in the subsequent month (say August). The GSTN does not allow the carry forward of ITC in such cases. Please suggest the solution.

ITC in your credit ledger will only be reflected after you have made an entry in “Eligible ITC” column of GSTR-3B, and only after that, you can claim the refund of ITC.

Dear Sir, provide the 1. meaning of Adjusted total turnover in GST Refund, 2. Turnover inverted rated supply in GST Refund.

1) “Adjusted total turnover” means the aggregate value of all taxable supplies (excluding the value of inward supplies on which tax is payable by a person on reverse charge basis) and exempt supplies made within a State or Union territory by a taxable person, exports of goods or services or both and inter-State supplies of goods or services or both made from the State or Union territory by the said taxable person but excludes central tax, State tax, Union territory tax, integrated tax and cess but excluding the value of exempt supplies other than zero-rated supplies, during the relevant period;

2) Inverted rated supply means GST rate on input supplies is more than the GST rate applicable on outward supplies i.e. a higher amount of ITC available against the lower amount of output GST liability.

I am trying to file Export refund according to the formula given by the GST site. But through that formula, I am getting only 80% refund which I suppose to get. Please guide how to move further.

Please check the formula you have applied since provisional refund of 90% of the amount is provided by the department within 7 days after the acknowledgement.

Dear Sir,

Kindly explain step for the refund amount.

Sir, we are providing business support services to an Australian Firm, when we are filing Form GST RFD 01A, in Annexure II – please can you explain what details have to be mentioned under :

EGM Details

BRC/FIRC

EGM stands for export general manifest which is a legal document which has to be filed by shipping carrier of goods once export takes place. In case, you are providing business support services. There is nothing to mention in EGM details as it is for goods only. While BRC/FIRC stands for Bank realization certificate or Foreign exchange realization certificate which is provided by the bank or authorized by the bank in case the foreign exchange is realized in Indian rupees. You have to fill the details of the certificate in this column.

MENTION TOTAL PURCHASES WITH GST PAID INVOICE TO INVOICE FOR EXPORTER

Plz clarify your query.

So adjusted total turnover does not include the exempt supply of goods and services but includes Zero-rated supplies right?

What is net input credit? If we have an input of some capital goods, can we claim it also as a refund? Also, my sale is 100 % Export.

There are different columns for IGST, CGST and SGST, we will mention same turnover and adjusted turnover in all? Please help

What is the meaning of “adjusted total turnover”?

Please guide..!!

“Adjusted Total Turnover” means the turnover that includes turnover of the state or Union territory, but it does not include the exempt supply of goods and services (except Zero-rated supplies).