It is essential for the registered individual to issue the tax invoice before or during the removal of goods for the supply of the recipient. To supply the services, the GST invoices could be provided prior to or post to the time of supply. Moreover, the e-invoicing system would have been executed within the phased method, which needs some important fields.

Latest Update

- The ICAI has published the third edition of its Handbook on Invoicing under GST. Read more

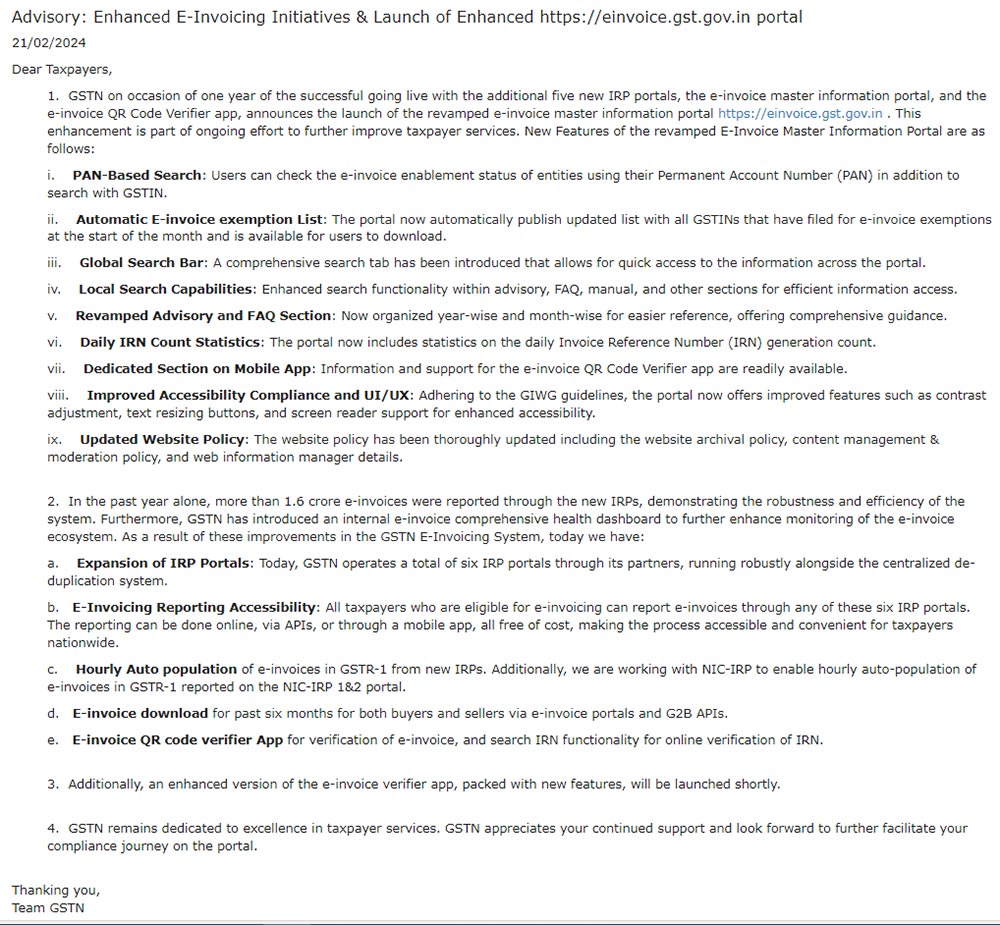

- GSTN has released an advisory to enhance and launch an improved official E-Invoicing Portal (https://einvoice.gst.gov.in). View more

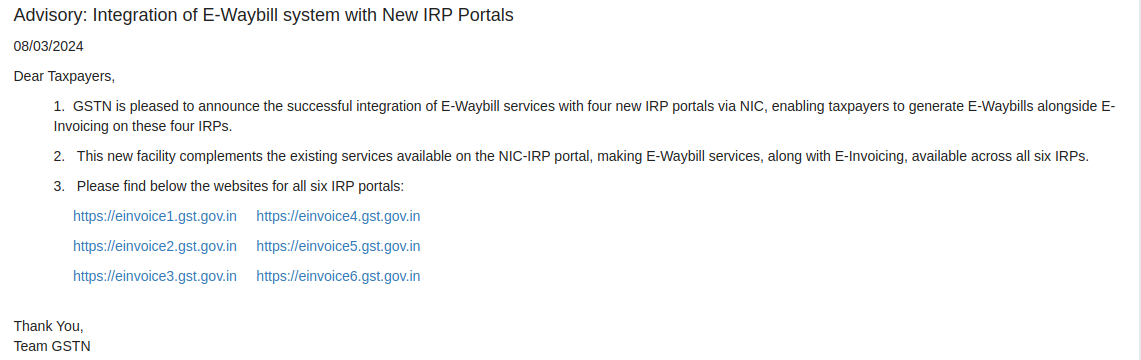

- The latest advisory pertains to the integration of GST E-Waybill services with four new IRP portals. View more

- The GSTN department has issued the advisory on four new IRPs which are providing E-Invoice services. View more View PDF

Details Mentioned in a Proper GST Invoice

Rule 46 of the CGST rules is concerned with the invoice contents. The tax invoice provided should transparently specify the data beneath the mentioned 16 headings-

- Supplier’s name, address, and GSTIN

- There shall be no more than 16 characters in the tax invoice number (it shall get generated sequentially and each tax invoice secured a unique number for that fiscal year).

- Issuance date

- When the buyer (recipient) is enrolled, the name, address, and GSTIN of the recipient

- When the recipient is not enrolled and the value exceeds Rs.50,000, the invoice must hold:

- Address and name of the recipient

- Delivery address

- State name and code**

- For the services, the HSN code of goods or service accounting code.

- Details of the goods or services.

- Goods quantity (number) and unit in UQC (metre, kg, etc.)

- Goods and services total value of supply.

- Post adjustment any discount on the taxable value of the supply

- Suitable GST rate (Rates of CGST, SGST, IGST, UTGST, and Cess clearly mentioned)

- Tax amount (With a breakup of amounts of CGST, SGST, IGST, UTGST, and Cess)

- Place of supply and destination name state for inter-state sales

- Delivery address when the same would vary from the place of supply

- If the GST would be levied on the reverse charge basis

- Supplier’s signature or his authorized representative

Indeed it gets deducted when the value is lower than Rs 50,000 merely when the recipient asks for the information.

The name of the country of the destination would be needed when the event is an export to the unregistered recipient with a value up to Rs.50,000.

From April 1st, 2021, HSN codes reporting would be as follows for the businesses.

- Turnover exceeding Rs.5 crore should use a 6-digit HSN code for all invoices

- The turnover lower than or identical to Rs 5 cr should utilize 4 digit HSN code for all the B2B invoices. For B2C invoices the same reporting would be a choice.

Earlier up to March 31st, 2021, the reporting was as follows for the businesses-

- Turnover lower than 1.5 crores- HSN code would not be needed to specify.

- Turnover between 1.5 -5 crores might utilize for a 2-digit HSN code

- Turnover above 5 crores should use the 4-digit HSN code

GST Invoice for Exports

Some invoices beneath GST should require endorsement or specified on the invoice. The case consists of the goods and services export and the supply to SEZ units or the developers to permit the functioning in the complied conditions-

- Using the tax payment

- Without using the tax payment under LUT or bond

For endorsement, the text would be of two kinds relying on the conditions provided above-

- Supply directed towards export/supply to SEZ unit or SEZ developer for authorized functioning on payment of integrated tax

- Supply directed to export or supply to SEZ unit or SEZ developer for authorized procedures beneath bond or letter of undertaking without payment of integrated tax

GST Invoice Bill Format

A tax invoice also called an e-invoice that comprises all the 16 essential fields beneath the GST shall appear like this-

GST officials might circulate around-

- For the goods or accounting code for the services and several classes, the registered individual must specify the number of digits of the HSN code.

- The registered person shall not be needed to specify the codes.

Causes for Not Providing the GST Tax Invoice

A registered individual might not provide the tax invoice if-

- The recipient would not be the registered individual and

- The recipient does not need these invoices.

Recommended: Step-by-Step Guide to Generate E-invoice Under GST with Benefits

Increases the Limit of GST Invoice Copies

The GST law needs businesses to maintain copies of all their invoices. The information on the same would be provided below. The invoices for the supply of goods, the invoices should be made in triplicate. They shall be precisely specified as

- Original Copy for the usage of the recipient

- Duplicate Copy for the usage of the transporter

- Triplicate Copy for the usage of the supplier

Invoices for the Supply of Services the invoice should be made in duplicate and should be cited as:

- Copy of Original for the usage of the recipient

- Copy of Duplicate for the usage of the supplier

GEN-GST is a full-featured software solution developed by SAG Infotech and is available on-premises as well as in the cloud. With the software, registered taxpayers can file unlimited returns. The software allows you to file, e-invoice, bill, and e-waybill, and it meets all of your compliance requirements instantly. At present, Gen GST software facilitates the filing of different forms for quarterly, monthly, and annual returns, such as GSTR-3B, GSTR 1, GSTR 9C, GSTR 9, etc.

{kind=link}

{kind=link}

{kind=link}