It was cited under the Gauhati High Court that the summary issuance of the Show Cause Notice in GST DRC-01 cannot replace the need for issuance of Show Cause Notice u/s 73(1) of the CSGT Act.

The Bench of Justice Manish Choudhury marked that “…….the issuance of the Summary of the Show Cause Notice, Summary of the Statement and Summary of the Order do not dispense with the requirement of issuance of a proper Show Cause Notice and Statement as well as passing of the Order as per the mandate of Section 73 by the Proper Officer. The initiation of proceedings under Section 73 and the passing of an order under the same provision have consequences. The Show Cause Notice, Statement as well as the Order are all required to be authenticated in the manner stipulated in Rule 26 [3] of the Rules of 2017.”

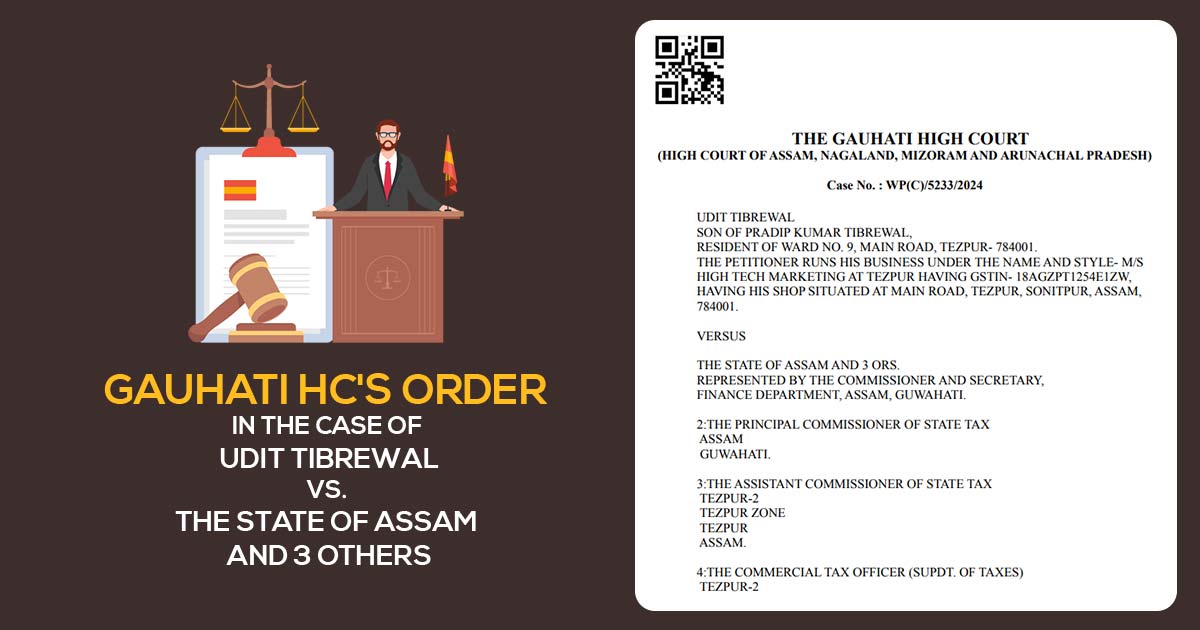

In this matter, the taxpayer has contested the order passed via the Commercial Tax Officer (respondent no.2) u/s 73 of the Assam Goods and Services Tax Act, 2017.

The taxpayer has contested the order based on the foundation that there was no effective and prior SCN stated under sub-section (1) of Section 73 of the Assam Goods and Services Tax Act, 2017 and the taxpayer was merely provided with a Summary of Show Cause Notice in Form GST DRC-01.

It was marked by the bench that the SCN summary in GST DRC-01 does not get replaced by the SCN to be furnished as per section 73(1) of the Central Act as well as the State Act. Irrespective of the issuance of the Summary of the Show Cause Notice, the Proper Officer would required to issue a Show Cause Notice to put the provision of Section 73 into motion.

As per Section 73 (1) of the Central Act or State Act the SCN is to be furnished and could not be confused with the determination tax statement which is to be furnished as per Section 73 (3) of the Central Act or the State Act, as perthe bench.

As per the bench “…….the attachment to the Summary of Show Cause Notice in GST DRC-01 is only the Statement of the determination of tax in terms with Section 73 (3). The said Statement of determination of tax cannot substitute the requirement for issuance of the Show Cause Notice by the Proper Officer in terms with Section 73 (1) of the Central or the State Act. Under such circumstances, initiation of the proceedings under Section 73 against the petitioners/assessee without the Show Cause Notice is bad in law and interfered with.”

| Case Title | Udit Tibrewal vs The State of Assam and 3 ORS |

| Citation | M.A.T. No.1595 of 2022 With I.A. No.CAN 1 of 2022 |

| Date | 25.10.2024 |

| Advocate for the Petitioner | Mr. A Goyal, Mr. A Choudhury |

| Advocate for the Respondent | Sc, Finance and Taxation |

| Gauhati High Court | Read Order |