Case Background: Chehak Fashions, a business that is in the trading of woven fabric, was served with a Show Cause Notice (SCN) dated September 20, 2021, for not filing returns for a continuous period of six months. The SCN was unclear, did not have the reasons, and did not specify the date and time for a personal hearing. Thereafter, on October 26, 2021, the GST registration of Chehak Fashions was cancelled with retrospective effect from July 26, 2017, with no furnishing of a clear rationale.

Procedural issues in SCN Issuance: Various procedural flaws have been noted by the Delhi High Court in the SCN issuance and the following order. SCN was not able to find out the detailed causes for the proposed cancellation. Also, the order on 26th October 2021 was the opposite since the same referenced a response from the applicant but cited that no response had been provided. The material proof absence to justify the retrospective cancellation was observed.

Statutes and Judge Interpretations: U/s 29(2) of the Central Goods and Services Tax (CGST) Act, 2017, a proper officer may cancel GST registration from a retrospective date if possibilities warrant such action. The court stressed that these cancellations must be based on the objective criteria and not just on the non-filing of the returns. The cancellation decision must acknowledge whether the action is required and justified under the situation.

The decision of the court: SCN along with the cancellation order does not have substantive justification and procedural fairness, the court noted. It was learned that both the applicant and the respondent agreed on the GST registration cancellation but for distinct causes. It is provided that the business operations have been ceased by the applicant and does not want to carry on the registration, the court altered the cancellation date to September 20, 2021, the SCN issuance date.

Closure: The ruling of the Delhi High Court in the matter of Chehak Fashions vs. Commissioner sets a precedent on the importance of procedural fairness and detailed justification in the GST registration cancellation. The same shows the importance of the tax authorities to comply with the criteria and furnish a clear cause when issuing the notices and making decisions that impact assessments.

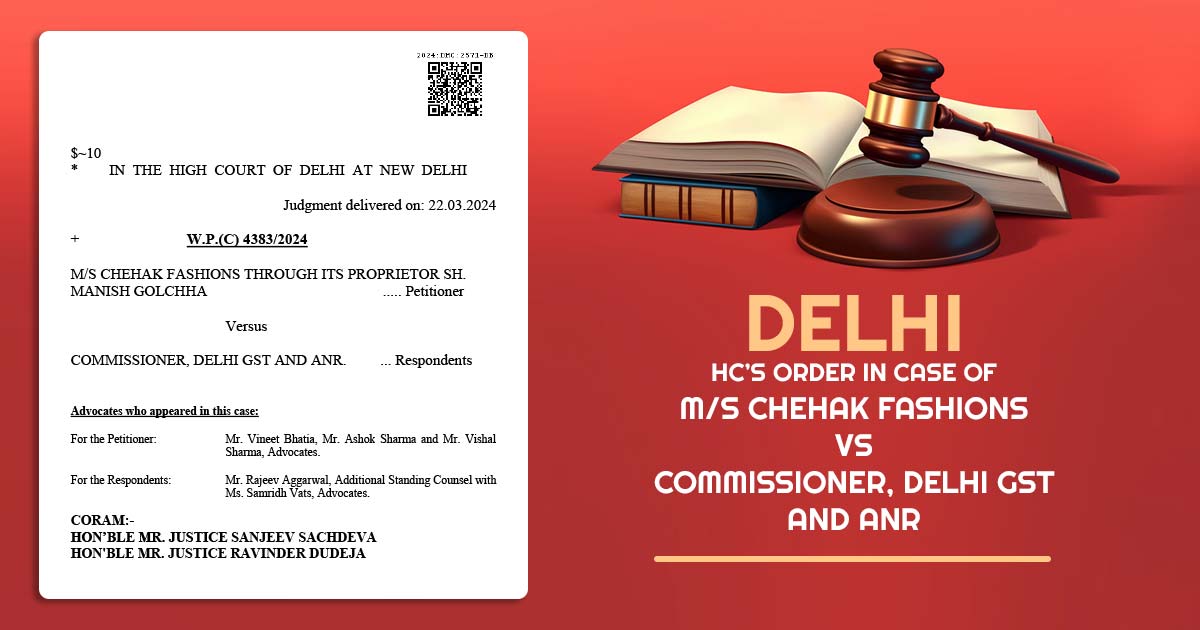

| Case Title | M/s Chehak Fashions Vs. Commissioner, Delhi GST and ANR |

| Citation | W.P.(C) 4383/2024 |

| Date | 22.03.2024 |

| For the Petitioner: | Mr Vineet Bhatia, Mr Ashok Sharma and Mr Vishal Sharma |

| For the Respondents: | Mr. Rajeev Aggarwal, Ms. Samridh Vats |

| Delhi High Court | Read Order |