The Chennai Bench of Income Tax Appellate Tribunal(ITAT) supported the ruling of the Commissioner of Income Tax (Appeals) concerning accounting manipulation and tax evasion due to insufficient evidence.

An appeal for Assessment Year (AY) 2015-16 has been furnished by the revenue appellant against the CIT(A) order on March 5, 2024, related to the assessment incurred via the Assessing Officer (AO) under Section 143(3) read with Section 153A of the Act, finalized on February 18, 2021.

The respondent-assessee, V.V. Titanium Pigments Pvt.Ltd, founded in 1994 and specializing in the production of titanium dioxide, was within a tax assessment following a search action on October 25, 2018. For various assessment years, notices were issued, prompting the company to file income returns.

Two major additions have been incurred via AO at the time of the assessment of the income of the respondent-assessee. First, the Assessing Officer (AO) alleged the manipulation of accounts based on an email from October 24, 2018, which proposed adjustments in stock and asset values, resulting in an addition of ₹1,930.36 lakhs for AY 2018-19.

Second, a cash discrepancy was reported, where ₹1.49 lakhs in physical cash was discovered, while the books recorded ₹0.93 lakhs, leading to a treatment of ₹0.56 lakhs as undisclosed income for AY 2019-20.

The Commissioner of Income Tax (Appeals) examined the additional tax assessments and found them to be unsupported by adequate evidence. The Commissioner emphasized that the email did not include incriminating evidence of tax evasion and only represented the opinion of the tax handler. The books of the taxpayer had been independently audited, and no negative findings were discovered for asset valuation or depreciation.

Prompting the revenue to file an appeal, CIT(A) removed the additions.

The ruling of CIT(A) has been kept by the tribunal claiming that the AO has not shown any tax evasion via a thorough examination of the books. It was again stressed that the email recommended the accounting adjustments and that no evidence connected the alleged manipulations to tax evasion.

Read Also: Mumbai ITAT Quashes Addition Due to Lack of Proof About Money Receipt from Seized Documents

The two-member bench including Mahavir Singh (Vice President) and Manoj Kumar Aggarwal(Accountant Member) discovered no reason to overturn the decision of CIT(A), dismissing the foundations which the revenue raised.

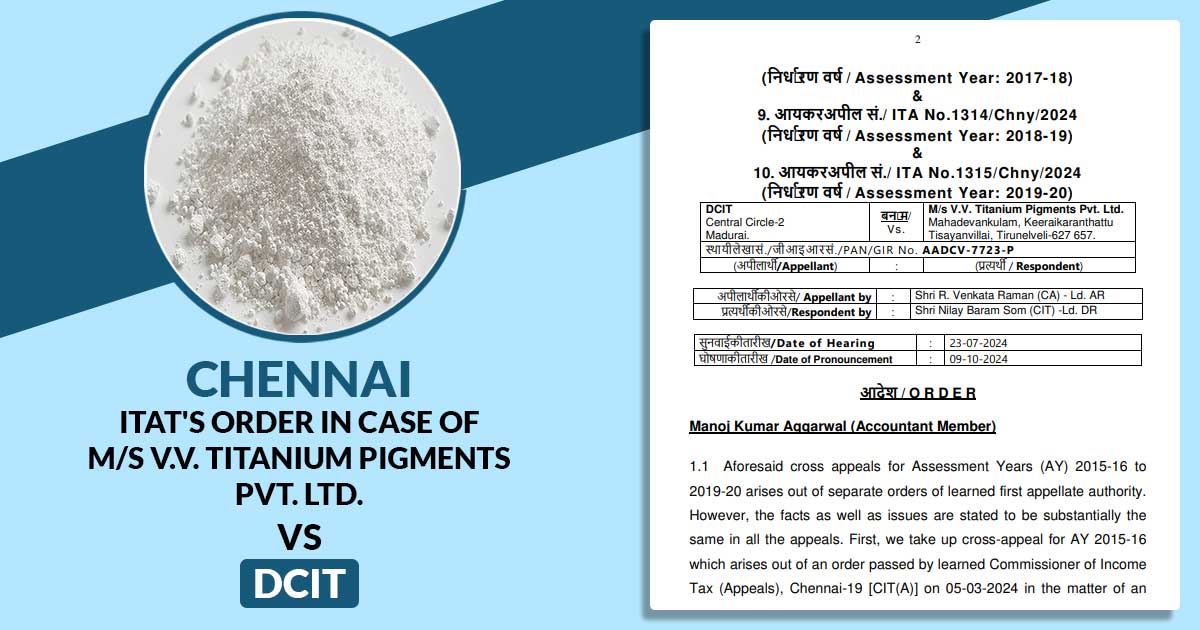

| Case Title | M/s V.V. Titanium Pigments Pvt. Ltd. Vs DCIT |

| Citation | ITA No.1315/Chny/2024 |

| Date | 09.10.2024 |

| Appellant by | Shri R. Venkata Raman (CA) |

| Respondent by | Shri Nilay Baram Som (CIT) |

| Chennai ITAT | Read Order |