The Input Tax Credit (ITC) under the mechanism of Goods and Service Tax plays a crucial role for a business and if it is mismanaged, it might adversely affect its working capital. And The GST Act 2017 has laid down a set of rules for claiming and utilizing ITC by every taxpayer.

Basics of Input Tax Credit?

It is better to start with zero. Firstly we need to understand what is Input tax credit. The Input tax credit simply means the amount that is paid at the time of buying raw material. A businessman can claim the Input Tax Credit

For Instance, if you purchase raw material (for instance ‘ink’ for a pen) from a registered dealer, you have to pay taxes on the purchase of ink. On adding value (by making a pen), you collect the tax by selling the pen in the market. Thereafter, you adjust the taxes that are paid at the time of purchase with the amount of output tax ( that is tax on sales) and balance liability of tax (tax collected on sales minus tax paid on the purchase of raw material) has to be paid to the government. This entire mechanism is called the utilization of input tax credit.

Issues to be Addressed Before Finalising Books of Accounts

Reconciliation of ITC Under GST

The amount of ITC that has been claimed by the assessee has to match with the details that are specified by the supplier in the concerned GST return. In case of any discrepancy, the supplier and recipient (who is claiming ITC) would be communicated of the same after filing of GSTR-3B

The filing of GSTR-3B and GSTR-2A is a crucial formality that has to be done by businessman claiming ITC. It assists businesses to claim

- Input Tax Credit

- Reverse any excess Input Tax Credit

That has been claimed. This entire mechanism if done in a proper way shall avoid the wastage of efforts done in sending demand notices by Income Tax Authorities.

Moreover, GSTR-2B was introduced first time in July-August 2020, and matching ITC” that has to be claimed in GSTR-3B with GSTR-2A” has now been shifted to a yearly affair.

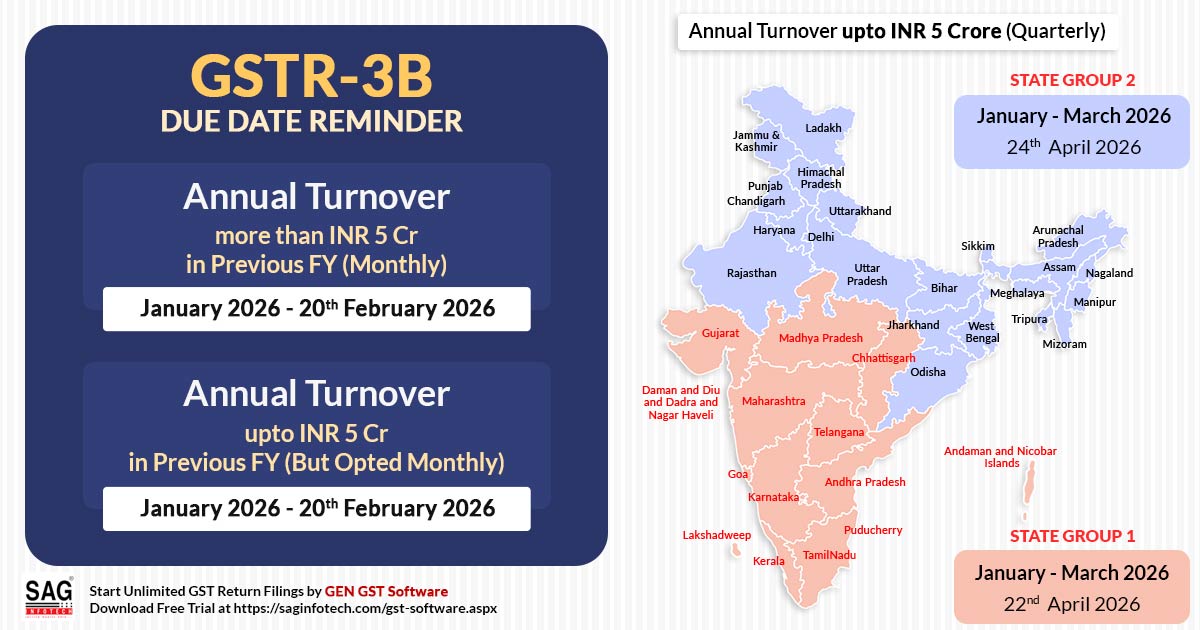

- GSTR-3B: GSTR-3B is a monthly summary return that is filed by the taxpayer by the 20th of the next month, 22nd or 24th of the month that follows the quarter

On the basis of details filled in Table 4 of Form GSTR-3B, taxpayer are granted permission to take and claim the ITC.

- GSTR-2A: GSTR-2A is an auto-populated form that is generated in the taxpayer’s login and covers all the outward supplies (Form GSTR – 1) declared by his suppliers.

Prerequisite of Reconciliation of Returns with the Books of Accounts

The Matching of the supplier returns with the books of accounts is necessary and better. Reconciliation ensures timely rectification of mismatches in the books of accounts of the taxpayer.

Reversal for Non-Payment

Section 16 of the CGST Act 2017 adds the conditions on the fulfilment of which ITC can be taken by a registered taxpayer. However, few restrictions have been put on availing of ITC in case the buyer or recipient of goods or services fails in making payment of consideration to the concerned supplier.

As per the second proviso to section 16(2) of CGST Act, 2017, the individual who is the recipient of goods or services is required to make the payment to the supplier within the purview of 180 days since the date of issue of the invoice. However, there is an exception — this condition is not applicable where tax is payable under the reverse charge mechanism.

In case, if the recipient of the goods or services has partially paid of consideration and tax within 180 days, then, he would have to make a reversal of ITC —on a proportionate basis for the aforesaid part of consideration and tax that has not been paid within 180 days.

Claiming Input Tax Credit on the Bank Charges

A statement that has been issued by a bank is treated equivalent to a tax invoice as per the prevailing GST law. The Input Tax Credit on bank charges is payable only if conditions that are mentioned in Section 16 of CGST Act,2017 are fulfilled.

Ineligible for ITC Claims

The GST Act 2017 specifically mentions several cases wherein input tax credit cannot be claimed. Nevertheless, if it is still claimed, then the taxpayer ought to reverse the same by paying it together with interest. For Instance, There are cases such as purchases made for personal use but accounted for in business books, ineligible for ITC. Moreover, Input Tax Credit on those capital goods that are sold before the expiry of five years from the date of buying attracts reversal that is based on percentage point reduction for the actual use of the assets.