The Calcutta High Court in a case asked the Commissioner of Central Goods and Service Tax (CGST) to file an affidavit to determine the validity of the Circular issued by the Central Board of Indirect Taxes and Customs (CBIC).

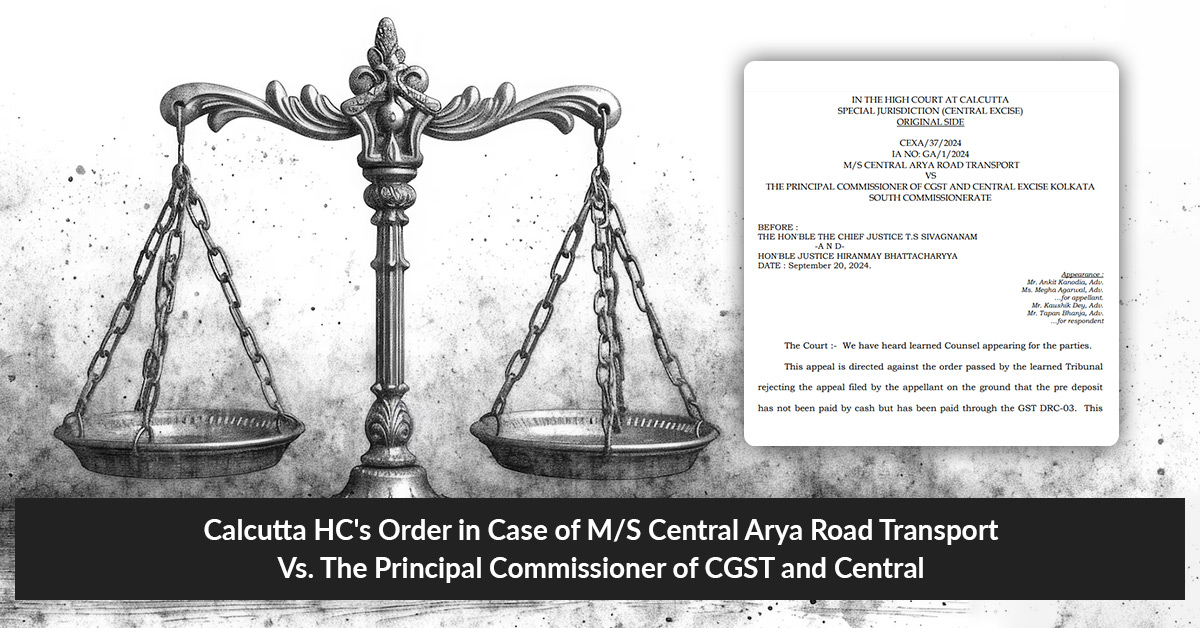

The applicant Central Arya Road Transport contested the order passed via the Tribunal cancelling the plea furnished via the appellant on the foundation that the pre-deposit does not get filed via cash however it has been filed via the GST DRC-03. As per the Tribunal, it is not permitted under the law and the pre-deposit would be required to be incurred as per the Finance Act 1994, read with the Central Excise Act, 1944.

The petitioner raised the question of whether Instruction No.CBIC-240137/14/2022-Service Tax Section-CBEC on 28.10.2022 issued by CBIC concerning pre-deposit payment method for cases about central excise and service tax wherein it was expressed that form GST DRC-03 is not a valid mode of payment for making pre-deposits is infructuous as there has been no rationale furnished via by the CBIC for such decision.

The first question of law contests the CBICs issued instruction on 28.10.2022 which appears to be pursuant to stated observations/directions issued via the Calcutta High Court of Judicature at Bombay in the matter of SODEXO INDIA SERVICES PVT. LTD. Versus UNION OF INDIA,2022 To determine this question of law the Court will need to go into the aspect if the issued circular via the CBIC is sustainable.

This decision can only be made after the appropriate authority files an affidavit in opposition. Therefore, the division bench, consisting of Chief Justice T.S. Sivagnanam and Justice Hiranmay Bhattacharyya, directed the respondent or any other appropriate authority with jurisdiction to file an affidavit in opposition where this affidavit should address the validity of the instruction by the CBIC dated 28.10.2022.

As the appellant has deposited the needed amount earlier hence the form GST DRC-03 and the mentioned amount has not been reversed via the department to date it would get retained as a deposit instead of cash payment since for the pre-deposit and the court shall take a judgment on the questions of law that was raised.

Read Also: Calcutta HC: Non-compliance with the Statutory Provision of Section 75(4) Invalidates the GST Order

The court scheduled the case for 22.11.2024 under the same heading. The respondents were asked not to take any coercive action against the appellant. Mr Ankit Kanodia, Adv., and Ms Megha Agarwal appeared for the appellant, while Mr Kaushik Dey, Adv., and Mr Tapan Bhanja appeared for the respondent.

| Case Title | M/S Central Arya Road Transport Vs. The Principal Commissioner of CGST and Central |

| Citation | CEXA/37/2024 and IA NO: GA/1/2024 |

| Date | 20.09.2024 |

| For Appellant | Mr Ankit Kanodia, Ms Megha Agarwal |

| For Respondents | Mr. Kaushik Dey, Mr. Tapan Bhanja |

| Calcutta High Court | Read Order |