The Calcutta High Court has set aside the case u/s 73(9) Central Goods and Services Tax (CGST) Act, 2017, because the consultant did not inform the petitioner of the Show Cause Notice (SCN) on the portal, and has remanded the case for fresh consideration, remarking that the consultant left the job without proper communication, thereby providing the applicants another chance to present their case and explain the situation to the proper officer.

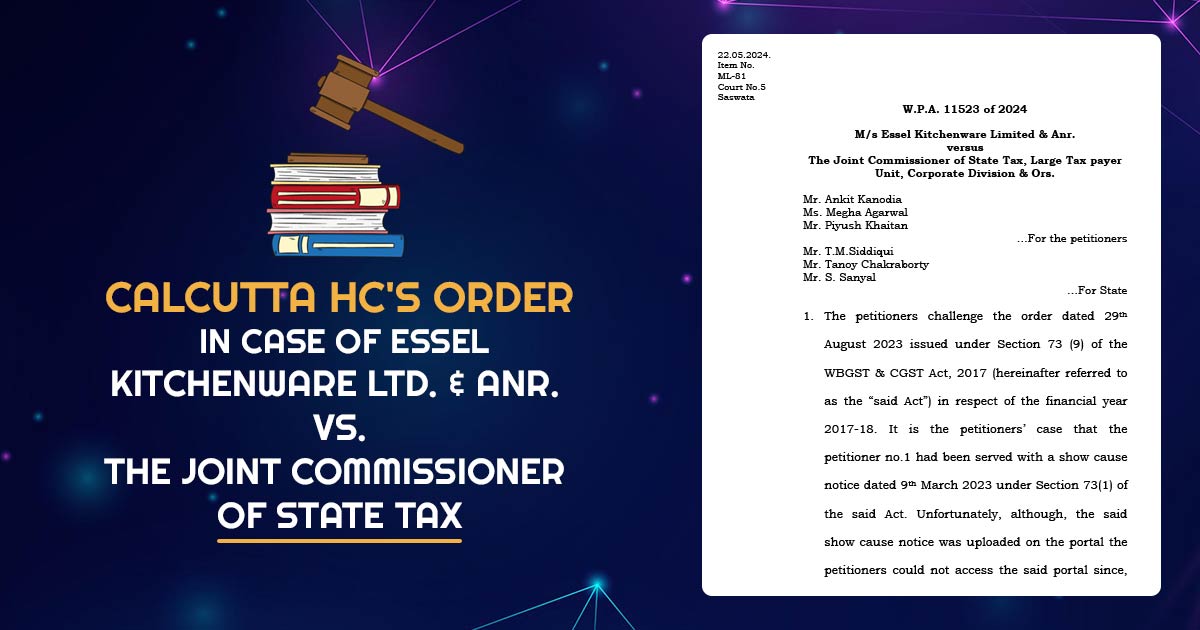

The applicants, M/s Essel Kitchenware Limited & Anr challenged an order on August 29, 2023, issued u/s 73(9) of the West Bengal Goods and Services Tax ( WBGST ) and Central Goods and Services Tax ( CGST ) Act, 2017, for the FY 2017-18. It was claimed by the applicant that applicant No. 1 had received a show cause notice on March 9, 2023, u/s 73(1) of the CGST Act.

They maintained that they could not view the GST notice on the portal since their consultant, who managed such tasks, did not communicate this information and subsequently resigned without informing them.

It was said by the applicant that they merely learned about the order on August 29, 2023, after hiring a new consultant. At the time of the proceedings, the advocate of the applicant Mr. Kanodia, cited that an error had emerged at the time of filing GSTR-3B for the FY 2017-18, where Input Tax Credit ( ITC ) on Import of Goods amounting to Rs. 2.94 crores was inadvertently reported in the wrong table.

The adjudication order remarked a discrepancy citing that the ITC on the import of goods in GSTR-2A is more than the claimed amount via the applicant in the correct table by Rs 2.93 crores. It was claimed by the applicant that they have rectified the same mistake in their yearly returns filed in Form GSTR-9, however, because they failed to present the same before the proper officer, it was not been taken into account.

Representing the State, Mr. Siddiqui, claims that the order in question was appealable and that the applicants can approach the appellate authority for redress.

Post hearing the arguments from both sides and analyzing the proof, the court considered that the appeared to be a genuine error on the applicant’s part, which has not been regarded by the proper officer. Remarking the departure of the consultant without proper communication the court wished that the applicants must be provided another chance to show their case and elaborate the situation to the proper officer.

The order was set aside by Justice Raja Basu Chowdhury of the single bench on August 29, 2023, and remanded the case back to the proper officer for reconsideration. 10 days were provided to the applicant to file their reply and the proper officer was asked to dispose of the proceedings via passing a new GST order u/s 73(9) within 4 weeks of the personal hearing.

The court ordered the applicants to pay Rs 50,000 to the State Legal Services Authority within 10 days and provide the payment proof during the hearing. The writ petition was disposed of subsequently.

| Case Title | M/S Essel Kitchenware Ltd. & Anr. Vs. The Joint Commissioner of State Tax |

| Citation | W.P.A. 11523 of 2024 |

| Date | 22.05.2024 |

| For the Petitioner | Mr Ankit Kanodia, Ms Megha Agarwal, Mr Piyush Khaitan |

| For Respondents | Mr T.M.Siddiqui, Mr Tanoy Chakraborty, Mr S. Sanyal |

| Calcutta High Court | Read Order |