What is Amnesty Scheme for GST?

The lenient non-filers and nil filers of GST returns will have a one-time Amnesty scheme from the government to deregister the GST (Goods and Services Tax) Council.

A senior tax official told, “Approximately there are 25 lakh ‘nil’ filer assessees while on an average 10 per cent of assessees have never filed returns so far”. These people do not give anything but add extra work to the tax system. He said, “A scheme for exit will bring relief to the taxpayers as it will bring down their compliance cost and at the same time there will be less pressure on the GST Network”. The government sometimes tries an amnesty scheme to increase compliance with the tax laws

As per the law, the person who is registered under GST has to file a return anyhow i.e. in any form. Return must be filed by the registered person either monthly (normal supplier) or quarterly (supplier choosing composition scheme). Monthly returns must be filed by an ISD (Input Service Distributor) and show the credit distributed details per month. The person who has to collect tax (TCS or Tax Collected at Source) and deduct tax (TDS or Tax Deducted at Source) have to file returns monthly showing the details of collected/deducted and other specified amount. Also, note that a non-resident taxable person has to file the return for the time period on no transaction

Latest Update

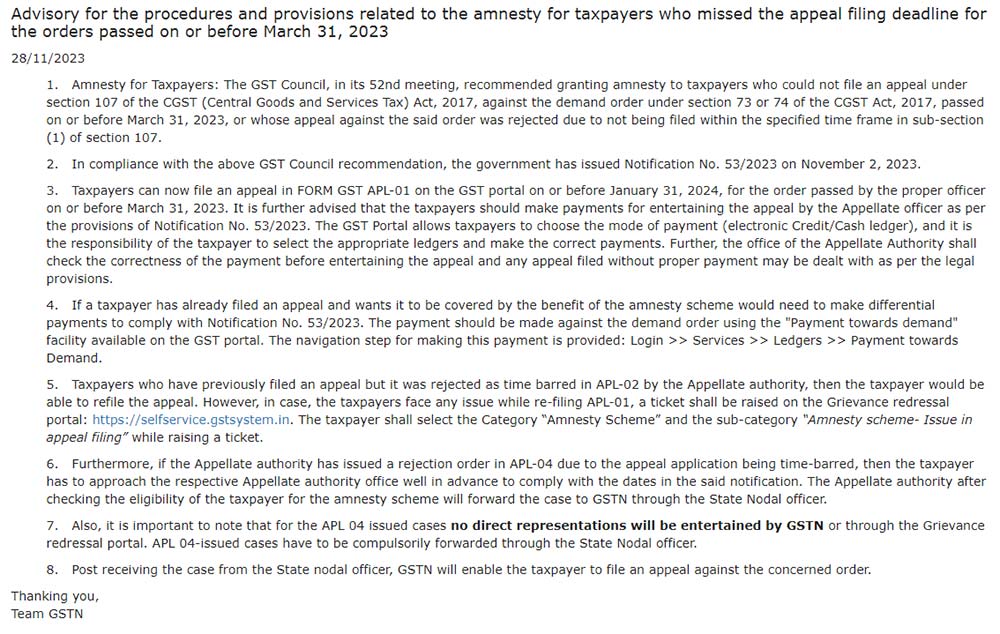

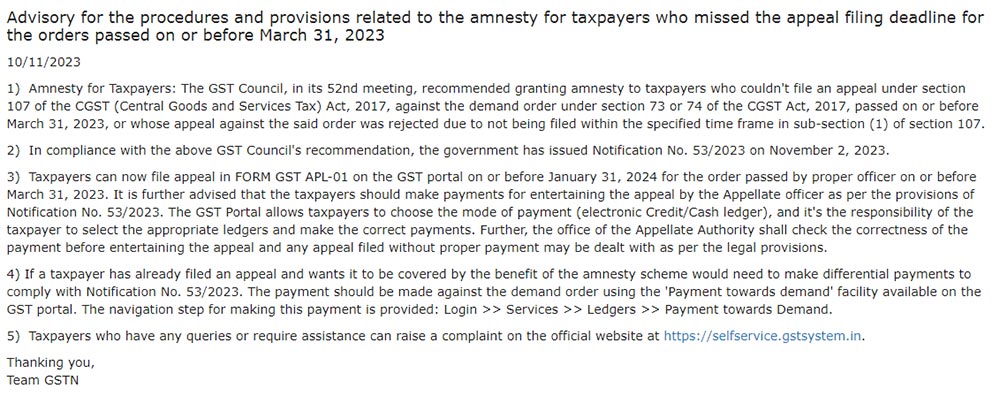

- The CBIC has recently announced important news related to amnesty provisions for missed appeal filing deadlines. This amnesty will apply to orders that were passed on or before March 31, 2023. View more

- This advisory provides information on the procedures and provisions related to the amnesty for appeals filed by taxpayers who missed the March 31, 2023 appeal filing deadline. View More

- An amnesty scheme under GST has been announced for taxpayers who can no longer appeal orders passed before 31 March 2023 or whose appeals have been rejected due to time limitations. Check all prerequisites here.

- The GST Amnesty Scheme extends the three-month appeal deadline until the end of January 2024 for all orders issued up until March 2023 with a 12.5% pre-deposit of tax, of which 2.5% is paid in cash. View more

- 50th GST Council Meeting: A void notification dated 31.03.2023 should be extended until 31.08.2023, in accordance with Section 62 of the CGST Act, 2017. This notification extends the amnesty scheme to non-filers of Form GSTR-4, GSTR-9, and GSTR-10 returns, registration cancellations, and deemed withdrawals of assessment orders. Read Press Release

- Gujarat High Court has ruled that when technical difficulties prevented the assessee from making the payment, the benefit of the amnesty scheme Sabka Vishwas (Legacy Dispute Resolution), 2019 cannot be denied to him. Read Order

Amnesty Scheme: Late Fee Norms for Defaulters Under GST

Any registered person who did not file the return has to pay the fine as punishment in the form of a late fee. If GSTR 3B is filed late then, the person must pay the late fee of Rs 50 per day i.e. in case of SGST and CGST (in case of any tax debt) Rs 25 per day and Rs 10 in each SGST and CGST (in case of Nil tax debt) i.e. Rs 20 per day subject to a maximum penalty of INR 5,000 from the given due date to the actual date when the returns are finally filed. It is said that the Amnesty scheme may provide relief from such fees.

Harpreet Singh, Partner at KPMG, said “Initial GST days resulted in a lot of non-compliances on account of lack of clarity of the law, frequent amendments, GSTN portal issues etc. Thus, an amnesty scheme, which can encourage genuine non-filers to suo moto come out and complete their backlog of non-compliances without any fear of penal consequences, would be a welcome step”.

Under GST, 1.16 crore people are registered as of now including the 64 lakh people who moved from the old system. Before GST reign, VAT/ST was the different pieces for registration in the State and was low as Rs 1 lakh which could reach up to Rs 20 lakh: the threshold for Central Excise was ₹1.5 crore and Service Tax was ₹10 lakh. As per the law, all such people were shifted to GST.

Singh said “Traditionally, amnesty schemes have generally resulted in increased compliance and tax revenues. However, the timing of the scheme, immunity from penal consequences and commitment to not initiate any investigations for those who participate in such scheme are some critical aspects on which the success or failure of the scheme hinges”.

Amnesty Scheme Approved by Meghalaya Govt for pre-GST Taxpayers

There was a Meghalaya cabinet meeting on Thursday and just after it, the Meghalaya cabinet approved an amnesty scheme. This amnesty scheme will help pre-GST taxpayers have outstanding dues to be paid to the government by availing of a 30% waiver.

Conrad K Sangma, Chief Minister, Meghalaya stated that the amnesty scheme will at one side help taxpayers with a 30% waiver, and on another side, it will also help the government as a way of revenue. He also appealed to taxpayers to get benefits of the amnesty scheme and also informed that this amnesty scheme will be valid for 6 months only.

Kerala Announces Amnesty Scheme 2020 for Clearing Pre-GST

Kerala government is giving the benefits to clear all the dues that were not considered in previous amnesty schemes like dues under Kerala Value Added Tax Act, Central Sales Tax Act, Tax on Luxuries Act, Kerala Surcharges Act, Kerala Agriculture Income Tax Act, and Kerala General Sales Tax Act. Dues shall be calculated from the date of submission of the option and all the dues shall be paid on the date of the option.

Assessees are barred from partial options (only for a particular period only). Those who opted for the earlier scheme but could not clear all the dues can apply for this amnesty scheme and partial payments (if made) in earlier amnesty schemes shall be credited to the existing scheme (only principal amount). For dues under Kerala General Sales Tax Act, the penalty is valid for dues before 1 April 2005 and in case of dues in-between 1 April 2005 to 31st March 2020 only the principal amount and interest will be charged. No penalty shall be imposed. ‘Revenue recovery process’ can be withdrawn by the tax authorities if the assessee has already opted for the amnesty scheme.

The due date for availing of the scheme is 31 July 2020. 60% less from the balance tax dues if they are paid in a lump sum and 50% in instalments. No refund is allowed under the scheme. 100% immunity from penalties.

{kind=link}

{kind=link}

{kind=link}

What is to be done in case Nil returns are filed for FY (no transactions) and GST returns filed in time. GSTR10 Filing delayed by two months. When i am trying to file GSTR10 . its showing a late fee of Rs 10000. What cam be done in such case? Whom to approach for waiver? Can i avail Amnesty scheme?

what about the GSTR 3B filing in the amnesty scheme whose GST numbers are cancelled,

how will they update their returns as it is more than 180 days their GSTN is suspended or cancelled suo moto

“Please contact to GST portal for the same”

It is a fact that lot of buisnesses were affected , due to GOI’s abrupt imposition of lockdown, throughout India. Many have to suffer due to the order, stay where you are. But, Finance ministry is not considering this implication and telling us to pay penaltyy for non compliance, for not filing returns. Day by day these charges are increasing, making many small scale institutions for going to bankruptcy. I Certainly think that government should give one time leniency for 2 years, else we need to close our business and go back to cultivating our fields, which I think is still not covered under gst. If the government don’t understand, that because of its uncalled upon harsh measures, businesses were killed. Sorry to say, but this government is very harsh on buisnesses.

I am consulting at Valsad our 4 clients are not cover all return after April 2020 to date. we request to announce to scheme to reduce the penalty to reduce late fees and also we recovered our professional dues. due to covid we unable to file all returns. also helpful to our family support for saver our fees.

I am from Karimnagar if Accountant or client must have their problems and some of the depression mode they file the return how they will file If this penalty with GST running the so many people will die so please understand the government if the monthly 500 is the penalty is okay everything to do. there are no getting government Jobs and how the public and people will live is not good for the GST

Amnesty scheme must be extended more uptown 31st march 2021 because pandemic is not yet over

Please raise your issue on the GST portal

I am an accountant. I pay 150000 late fees now 10 party returns pending plz save my life provide GST amnesty scheme from July 17 to Jan 21

I am working as an accountant in a (P) Ltd. company. Due to certain official issues, we can’t file the return in the time since 2017 Sept. May I get a chance to get amnesty for filing the return or not. Please give me your answer at the earliest. Favourable action from your side is much apprecialble.

Sir, 17.01.2020 is the last date to file GSTR-1 for the period July 2017 to Nov 2019

33rd GST Meeting announces up to GSTR3B AND GSTR4 LAST DATE 31.03.2019.

As per recommendations made in 31st GST council meeting, the department has waived late fees for GSTR-1, 3B & 4 for the period of July 2017 to Sep 2018 if the returns for the said period are filed on or before 31.03.2019.

SIR, I HAVE NOT FILED RETURN FROM NOVEMBER 2017 TO TILL MONTH BECAUSE THEY HAVE A HUGE LATE FEES. THIS LATE FEES ARE WAIVED FROM AMNESTY SCHEME? HOW WAS DATE OF LAUNCH AMNESTY SCHEME FROM GST PORTAL? PLEASE, SIR, I AM WAITING FROM YOUR REPLY.

I am already paid penalty 25k, then what about my money, is to be refunded or not?

If not, then I think its better to late filling with amnesty scheme form.

It will not be refunded. Yes, it is a better option either.