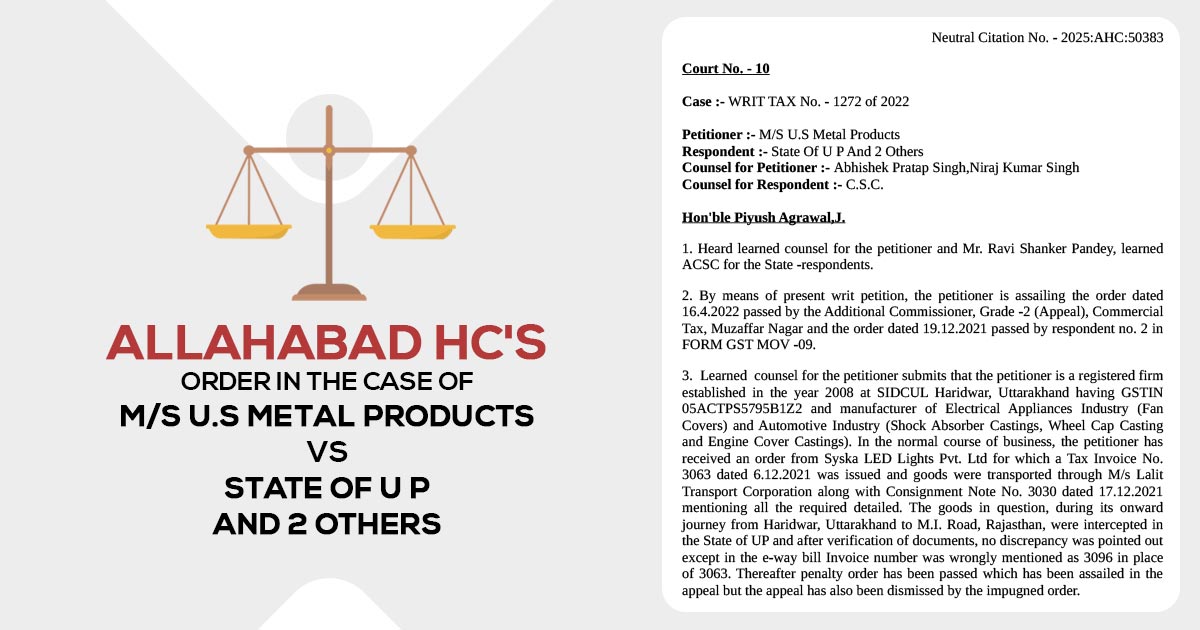

The Allahabad High Court has made a significant ruling regarding minor clerical errors in documentation related to the Goods and Services Tax (GST).

The court determined that discrepancies such as a one or two-digit mismatch in GST invoices or on the GST e-way bill should not serve as grounds for initiating legal proceedings under Section 129 of the Central Goods and Services Tax (CGST) Act of 2017.

The production of components for the electrical appliances and automotive industries is the business of the petitioner, a manufacturing firm based in SIDCUL, Haridwar, Uttarakhand.

The petitioner dispatched goods to Syska LED Lights Pvt. Ltd., including a valid tax invoice (No. 3063 dated 06.12.2021) and appropriate transportation documents.

In Uttar Pradesh, the goods were intercepted which was in transit from Uttarakhand to Rajasthan. All documents were in order, but the e-way bill erroneously mentioned the invoice number as “3096” instead of “3063”.

The State Tax Officer imposed a penalty u/s 129(1)(a) of the CGST Act, 2017, even after having this minor error.

Additional Commissioner (Appeals), Muzaffarnagar, dismissed the appeal of the applicant against the penalty. The applicant approached the HC by not satisfied with both orders.

The petitioner referenced Circular No. 64/38/2018-GST, issued on September 14, 2018, with particular attention to clause 5(d). This clause states that when goods are transported with valid documentation and an e-way bill, authorities should not initiate proceedings under Section 129 for minor discrepancies. Such minor errors may consist of variations of just one or two digits in the document number.

No discrepancies were there in the quantity, quality, or type of goods during verification; a typographical mistake was only there in the invoice number, Justice Piyush Agwrwal said.

The court said that issued circulars via the Central Board of Indirect Taxes and Customs (CBIC) are binding on field officers, expressing the Supreme Court’s rulings in Commissioner of Central Excise v. Ratan Melting & Wire Industries and Commissioner of Central Tax v. Gurukripa Resins Pvt. Ltd.

The penalty orders were quashed by the Allahabad High Court on 16.04.2022 and 19.12.2021, and it ruled that the whole proceedings against the applicant were unsustainable under the regulations. It asked that any deposited amount of the applicant for the same should be refunded as per the law.

| Case Title | M/S U.S Metal Products vs. State Of U P And 2 Others |

| Case No. | WRIT TAX No. – 1272 of 2022 |

| For The Petitioner | Abhishek Pratap Singh, Niraj Kumar Singh |

| For The Respondents | C.S.C. |

| Allahabad High Court | Read Order |