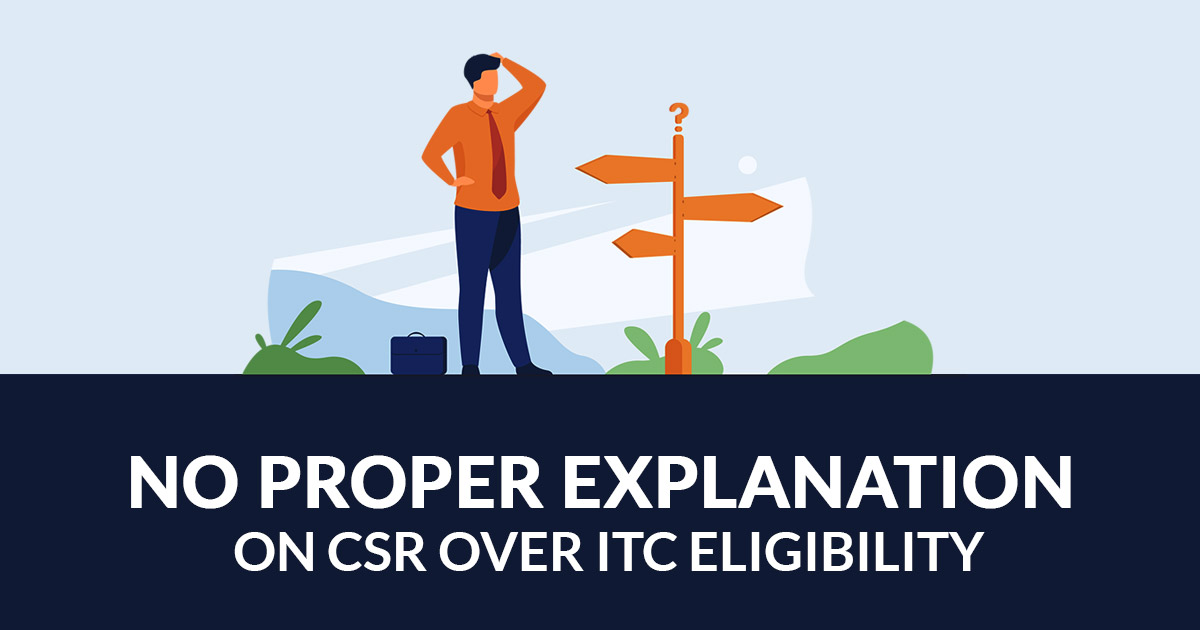

Beneath the goods and services tax (GST) regime the Contradictory corporate social responsibility (CSR) judgments by the Authorities for Advance Ruling (AARs), have made confusion inside the private players who had been not happy with the laws.

In recent times the Uttar Pradesh AAR ruled that CSR has to spend through the firms is liable for the input tax credit (ITC)

Towards the event of Dwarikesh Sugar Industries, which has the business of manufacture and sale of sugar and allied products, the firm undergoes several CSR activities. This consists of the construction of school buildings, free supply of furniture, and free supply of electrical goods for use in school.

For the provision of these goods, the petitioner availed that GST was summoned through the supplier and wanted to determine if it was liable for the input tax credit. UP AAR mentioned that CSR expenses are made important through the companies act 2013 and is the responsibility of the petitioner to sustain an expense so as to complain in the law.

under Section 17(5) of the Central GST (CGST) Act. According to Section 17(5) of the CGST Act, the CSR expenses are not sustained voluntarily, they will not succeed as gifts. Thus credit will not be limited the input tax credit is not made present for the goods lost, stolen, or provided as free samples or gifts. The UP Authority of Advance Rulings (AAR) has held that the company will be liable for the input tax credit for sustaining the CSR spend.

However, for the case of Polycab wires who has provided the electrical items such as switches, fans, and cables to flood-affected people beneath the CSR expenses for free, the Kerala AAR held that “for these transactions, the input tax credit will not be available”

The organizations had given the goods free of cost to Kerala state Electricity Board (KSEB) for restoring connectivity in the flood-affected places as it is part of the ‘mission reconnect’ a CSR activity. The distributors have provided the tax invoices to KSEB which show the sale value, GST, and the total amount through a 100% discount.

But GST Liability was Furnished to the Govt

The petitioner has shown that since GST liability was fully paid, free supplies are liable to claim the full input tax credit claim. As per that the companies act the company whose net worth of Rs 500 cr or exceed or the turnover of Rs 1000 cr or the profit of Rs 5 cr or exceed in any fiscal year is important to spend for 2% of the average net profit for CSR activities every financial year.

CSR Various Contradictory Rulings by AARs

Moreover, classification issues, revenue biases in rulings, delays in disposing of applications and lack of senior officers in AARs have made the advance ruling mechanism under GST unpopular among industry players.

The contrary AARs if the input tax credit is to be subjected upon the CSR spent through the companies which have made confusion in the industry peoples said Abhishek Jain EY.

“Considering that most companies provide free goods under their CSR agenda to ensure compliance under the Companies Act and is clearly a business expense, the government should provide explicit clarity if input tax credit would be available in case of procurement of goods for CSR. It should align the GST law accordingly”, said Jain.

AARs include joint commissioners or additional commissioners of state governments and the central government.